.jpeg)

Average Restaurant Profit Margin: The Benchmark by Segment and Why Yours Might Differ

Average Restaurant Profit Margin, by Segment

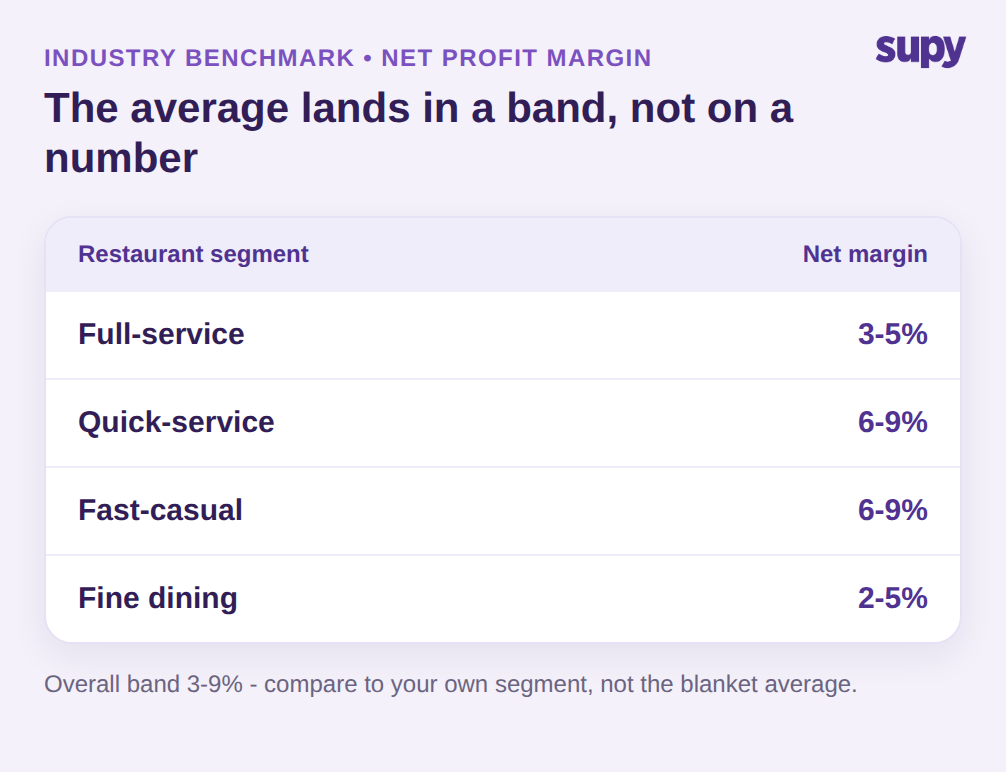

Across published industry benchmarks, the average restaurant profit margin lands in the 3-9% band of revenue. That headline range is real, but it hides more than it reveals, because net margin varies sharply by format. Full-service restaurants typically run 3-5%. Quick-service and fast-casual concepts typically run 6-9%, helped by lower labour intensity, simpler menus, and faster turns. Fine dining often sits at the low end, around 2-5%, because high menu prices are offset by expensive ingredients and heavy labour.

So the first useful move with any average restaurant profit margin figure is to stop treating it as a target and start treating it as a reference point for your own segment. A 5% net margin is unremarkable for a fine-dining room and a warning sign for a quick-service brand. The benchmark tells you which conversation you should be in; it does not tell you whether your own number is healthy. To decide that, you have to know exactly which margin you are measuring and what is dragging it down.

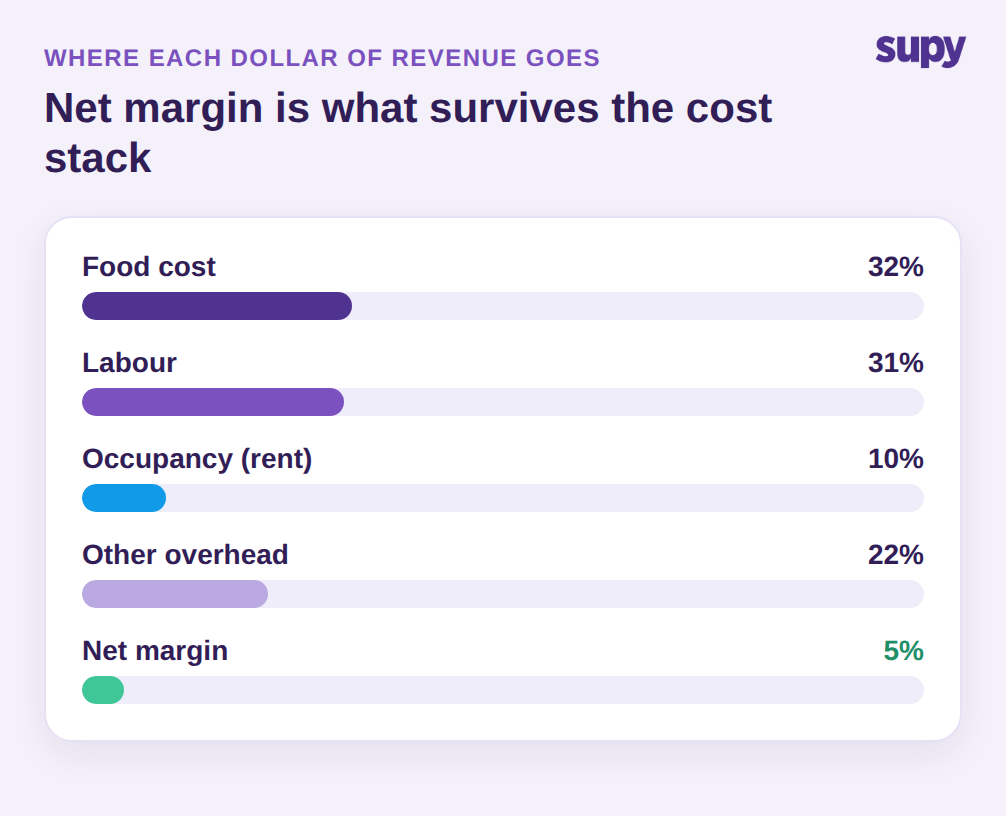

It also helps to remember what a net margin actually is before you compare yours to anyone's. Net margin is profit after every cost, expressed as a share of revenue, which means it is the thinnest and most fragile number on the P&L. On a 5% net margin, five cents of every dollar survives; a two-point slip in food cost can halve it. That fragility is exactly why a single blended benchmark is a weak tool and why the rest of this guide focuses on where your own number is built and where it leaks.

Gross Margin vs Net Margin: Which Number Are You Comparing?

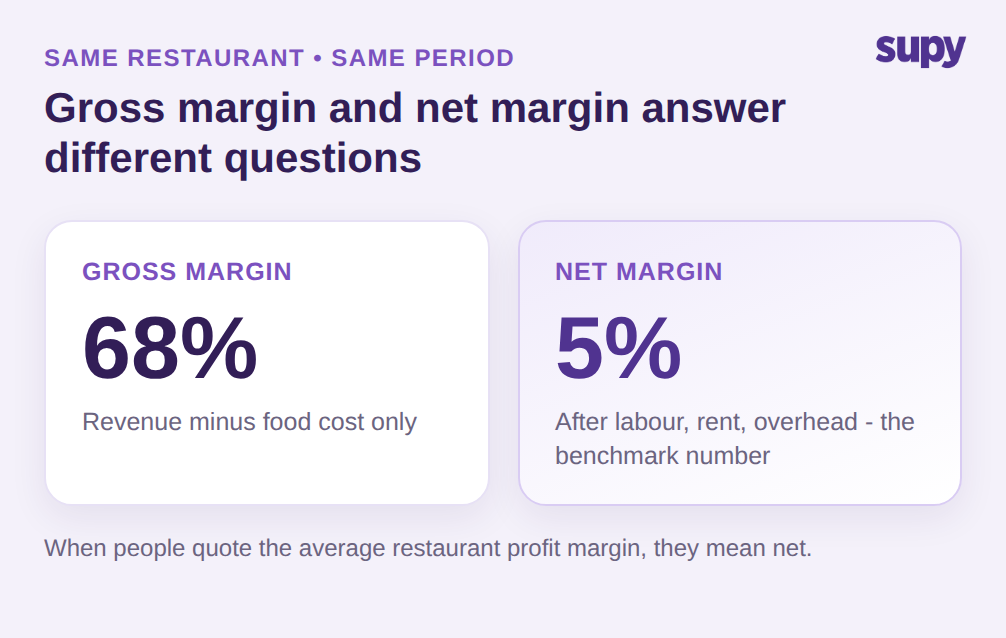

Most benchmark confusion starts here. Gross margin is revenue minus the cost of the food itself, and it usually looks healthy, often around two-thirds of sales. Net margin is what remains after everything else: labour, rent, utilities, marketing, and overhead. The same restaurant can show a 68% gross margin and a 5% net margin, and both are correct because they answer different questions. When people quote the average restaurant profit margin, they almost always mean net. For the gross side of the picture in detail, see our guide to restaurant gross profit margin.

There is a second definition trap that multi-channel operators hit constantly: what counts as revenue. One group running dine-in and delivery found its finance team and its operations team reporting different margins for the same business, because finance used gross revenue including delivery-platform fees while operations excluded the commission. Neither was wrong, but they were not comparable, and neither matched the benchmark cleanly. Before you compare your number to any average, settle the denominator: is delivery counted at gross order value or net of commission? Get that wrong and you will chase a gap that is really a definition difference.

The distinction matters more than it sounds, because delivery has quietly reshaped the margin maths for a lot of operators. A delivery order can carry the same food cost as a dine-in cover but arrive with a fifth or more of its value taken in platform commission before it reaches the P&L. A brand that has grown its delivery mix without re-checking its margin definition can look like it is missing the benchmark when the real story is channel mix, not operational weakness. The fix is not to abandon delivery; it is to measure each channel's true contribution margin separately, so the blended net figure is understood rather than blamed. Only once gross and net, and dine-in and delivery, are cleanly separated does comparing yourself to the average restaurant profit margin tell you anything at all.

Why Your Real Margin Sits Below the Benchmark

Once the definitions are settled, the structure of restaurant costs explains most of the gap between the benchmark and your bank balance. Food cost typically runs 28-35% of sales and labour another 28-35%, which is why operators track prime cost (food plus labour) and aim to keep it at or below roughly 60% of sales. Net margin is simply what survives after prime cost, occupancy, and overhead, so a few points of drift on either food or labour is the difference between a healthy number and a thin one.

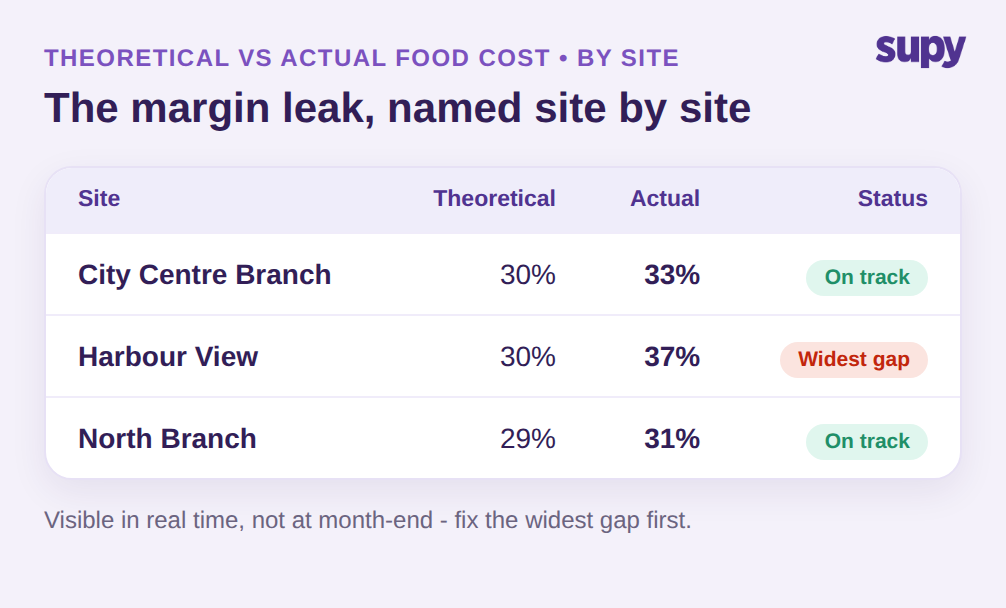

The problem is that the margin most operators believe they run is theoretical, not actual. Theoretical margin is built from standard recipe costs and menu prices; actual margin is what the P&L reports at period end. A head of operations at a multi-location fast-casual chain found the two diverged by a consistent 4-5 points, traced to recipe costs that no longer reflected real purchase prices. Every time a supplier price rises and the recipe cost is not updated, the theoretical margin drifts above reality, and the operator only discovers the true figure at month-end, too late to act on that period. That is why comparing a stale theoretical margin to a benchmark is misleading in both directions. Our guide to theoretical vs actual food cost variance works through how to isolate where that gap comes from.

Food cost is usually the fastest-moving of the two prime-cost lines, which is why it deserves the closest watch. Menu prices are reset a few times a year; ingredient prices move every week. A restaurant holding menu prices flat through a season of supplier increases will watch its food-cost percentage climb and its margin fall, even though nothing about the menu or the operation appears to have changed. Tracking food cost percentage against a target per recipe, per site is the difference between catching that drift in week two and finding it in the quarterly numbers. The benchmark net margin you are chasing is downstream of this one discipline more than any other.

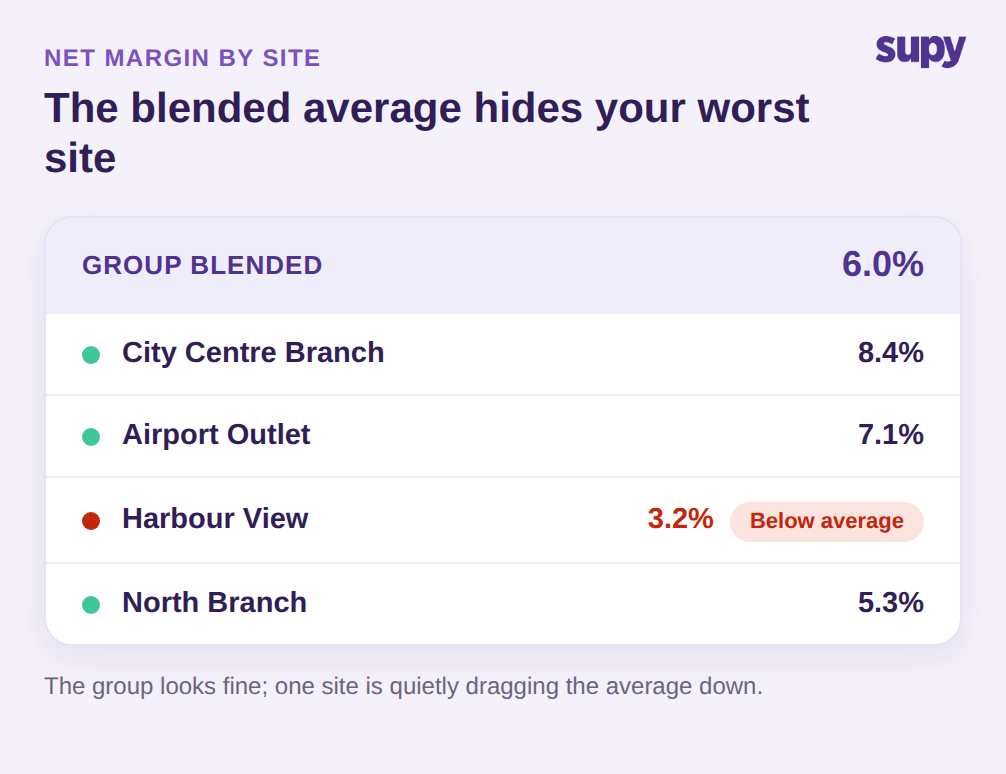

The Multi-Site Trap: How a Blended Average Hides Your Worst Sites

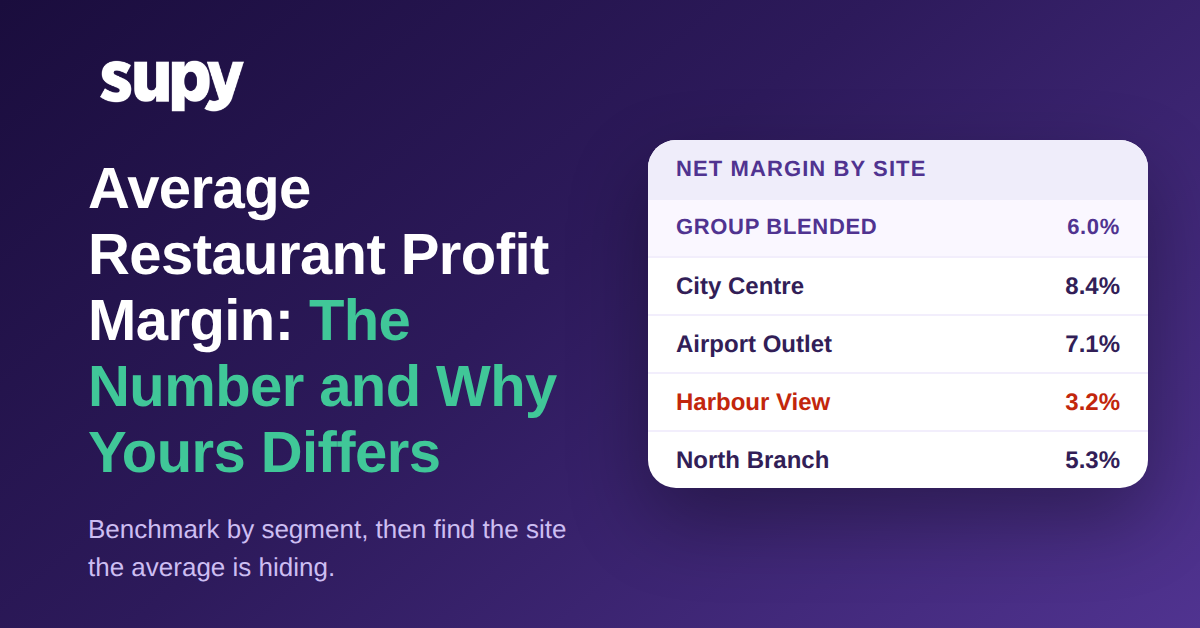

For a group, the single most dangerous number is your own blended average, because it behaves exactly like the industry benchmark: it smooths over the sites that need attention. A multi-site casual-dining operator's finance team reported a steady blended margin across the group and treated it as proof of stability. A quarterly deep-dive found two sites running several points below the rest; the healthy locations had been carrying them, and the blended figure delayed the fix by a full quarter.

This is the core reason a company-wide average restaurant profit margin is close to useless for a multi-site operator. A group sitting comfortably on its blended margin can easily contain one site several points below it and another several points above, and only the site-level view tells you where to intervene. The benchmark question for a group is never simply "are we above average?" It is "which sites are below our own average, and by how much?" Averages, whether the industry's or your own, are where underperformance goes to hide.

The reason this trap is so common is that most reporting rolls up before it drills down. A monthly P&L pack lands as a group total, the blended margin looks close enough to the benchmark, and no one asks the site-level question until a location is in real trouble. By then the group has carried the weak site for months, and the recovery is far harder than a small correction would have been at the first sign of drift. Seeing margin by site, every period, is what converts the benchmark from a vanity number into an early-warning system.

The Levers That Actually Move Net Margin

Raising prices and cutting portions are the advice you will find everywhere, and both erode the guest experience before they move the margin much. The levers that move net margin without touching the menu are operational, and they all depend on seeing the real numbers by site. This is where Supy fits, through inventory management that turns the theoretical-versus-actual gap into something you can act on during the period, not after it.

Supy dashboards calculate theoretical food cost from actual recipe sales quantities and current ingredient costs, then compare it to actual usage, so the gap that quietly costs you points of margin is visible in real time rather than at month-end. Wastage cost is tracked for both individual items and full recipes, giving the cost of spoilage and over-production by branch and period, which is a direct net-margin lever most groups cannot even measure. Because every figure is available per site, the blended average stops hiding the underperformers: you can see which location is running a wider food-cost gap or higher waste and fix that one, instead of nudging prices across the whole group. Each of these is a live capability, and together they turn "our margin is below benchmark" into a specific, per-site action list.

So use the benchmark as a starting line, not a finish line. First, place yourself: compare your net margin to your own segment's band (3-5% full-service, 6-9% quick-service and fast-casual, 2-5% fine dining), not the blanket 3-9%. Second, stop looking at the blended number and rank your sites by net margin, so the ones below your own average are named. Third, on each low site, measure the theoretical-versus-actual food-cost gap; a 4-5 point gap is a period's worth of margin sitting in stale recipe costs and unrecorded waste. Fix the widest gap first. The average restaurant profit margin only becomes useful the moment you stop comparing yourself to the industry and start comparing your sites to each other.