.jpg)

The 4 Points Where Supplier Credit Notes Go Missing in Multi-Site Restaurant Groups

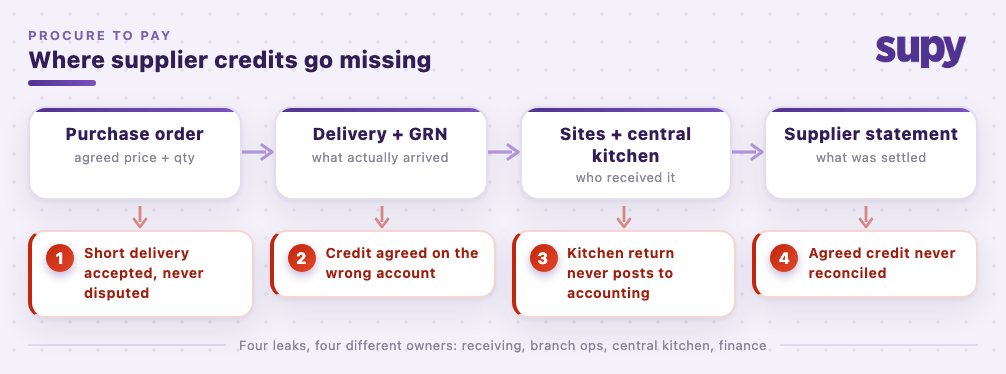

Where do supplier credits actually go missing?

Supplier credits leak at four points: at receiving, when a short or substituted delivery is accepted without a dispute; between sites, when a credit is agreed against the wrong location's supplier account; at the central kitchen, when returns to suppliers never reach the accounting system; and on the statement, when an agreed credit is never reconciled against what the supplier actually applied.

Each leak has a different owner, which is why chasing "missing credits" as one problem fails. The scale of the mess is easy to underestimate because each individual credit is small. In one systems review, a multi-location operations lead listed seven distinct receiving and credit-note gaps in a single session. A finance manager at a multi-location group described supplier credit handling as effectively absent from their procurement workflow: credits lived in email threads and delivery-note margins, not in any system finance could reconcile. None of this is carelessness. The four points sit in four different teams' blind spots, and no single person sees the full path from a short delivery to a settled statement.

At receiving: the short delivery that never becomes a dispute

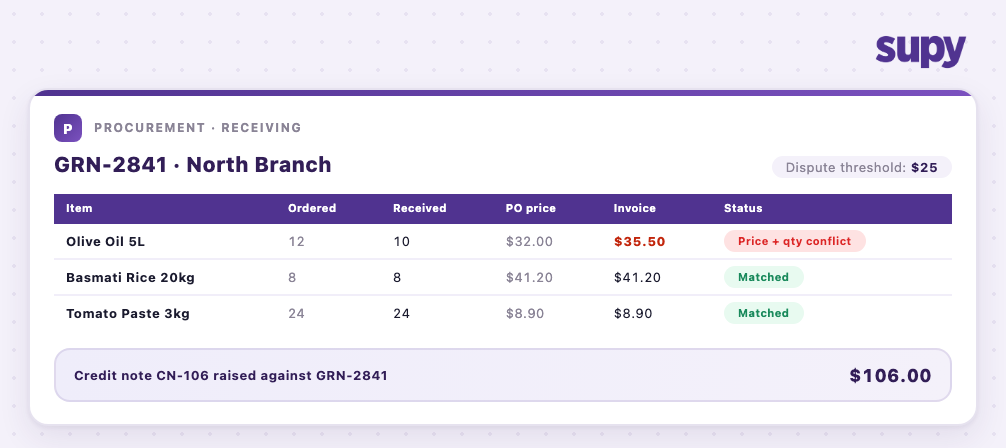

A credit is born at receiving, or it usually is not born at all. If the goods received note (GRN, the record of what physically arrived) does not capture the gap between what was ordered and what came off the truck, the supplier's invoice becomes the only record, and the credit never exists.

Receiving conditions work against accuracy: early-morning deliveries, weight-variable produce, one person checking forty lines while the driver waits. The arithmetic still adds up. As a purely illustrative example, take a site receiving 200 deliveries a month. If 4% arrive short by an average of $18, that is $144 a month leaking at one site, $1,728 a year, and across a 12-site group over $20,000 in credits that were never claimed. Every figure there is a worked example, not a benchmark; the point is that per-delivery amounts too small to chase individually compound into real money.

Closing this leak is a workflow question, not an effort question. A receiving flow that holds the line does four things: it converts the purchase order to a GRN in one step, so there is always a baseline to compare against; it lets the receiver edit quantity and price at the door, while the evidence is still on the scale; it flags price and quantity conflicts against the purchase order automatically instead of relying on memory; and it raises the credit note against the GRN itself, so the dispute and the delivery record are one object. Two guardrails stop the noise from drowning the signal: a dispute threshold, so credits fire on the $80 gaps and not the $0.40 rounding differences, and a cap on additional charges per GRN, so a delivery fee cannot quietly absorb a line discrepancy. For weight-variable produce, item-level tolerances do the same job: a workable starting point is a tight tolerance on packaged goods and a looser one on fresh items, adjusted once you can see your own dispute history.

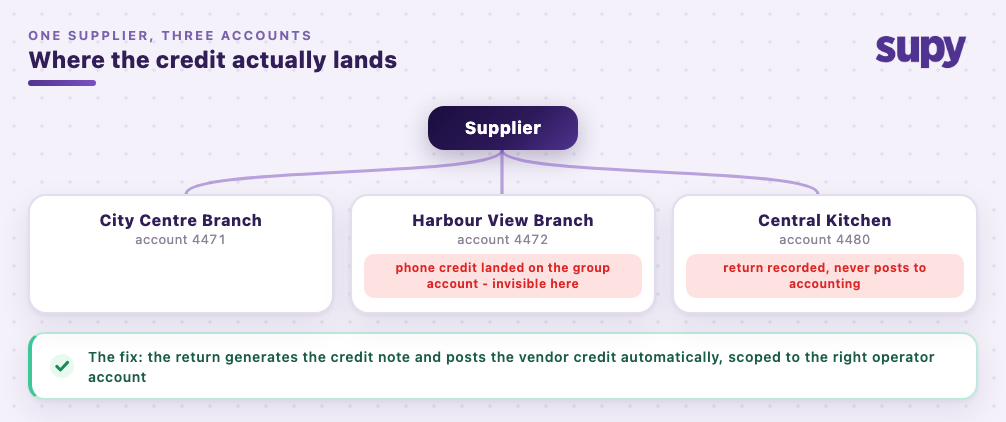

Between sites and the central kitchen: credits on the wrong account

In a group, the question is never just "did we get the credit" but "did the right entity get it". Multi-site groups usually hold a different supplier account number per location, and a central kitchen both receives from suppliers and ships to its own sites, so a credit raised in the wrong place lands on the wrong books and disappears from the view of the person chasing it.

Two failure modes dominate. The first is the phone-call credit: a branch manager agrees a credit with the supplier's driver or rep, the supplier applies it to whichever account their system defaults to, and the branch that suffered the shortage never sees it. The second is the central kitchen blind spot: one central kitchen operations lead described supplier returns raised at the kitchen that never reached the accounting system at all; finance only discovered the gap weeks later, during statement reconciliation, when the supplier's balance and the group's books refused to agree.

The fix is structural. When a supplier return is recorded in a system built for group operations, the return itself generates the credit note and pushes it to the connected accounting system as a vendor credit, so the paper trail exists whether or not anyone remembers to follow up. And credit notes are scoped to a single operator account, which means one brand's supplier credits cannot mix with another's even when the same supplier serves both. Between those two mechanisms, "who got our credit" stops being a research project.

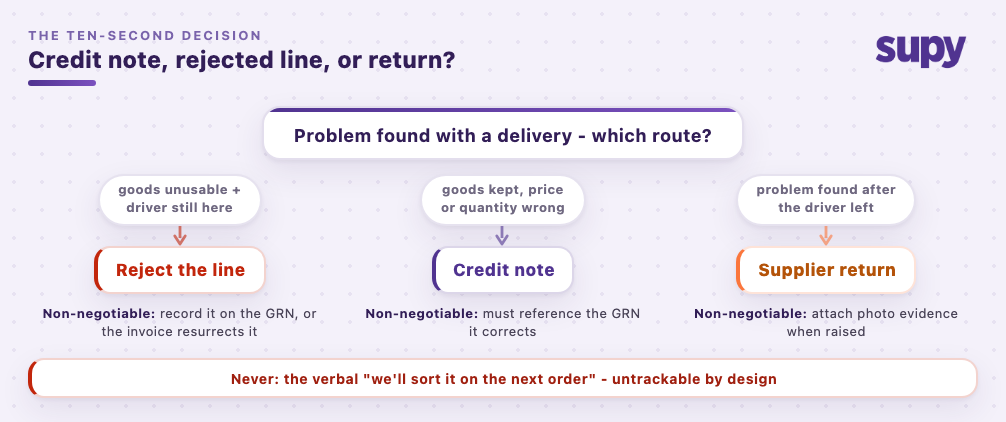

Credit note, rejected line, or return: choose in ten seconds

The decision at the moment of discovery is simpler than most teams make it. Reject the line at the door when the goods are unusable and the driver is still there: no credit note needed, because the corrected invoice should never include the line. Take a credit note when you keep some or all of the goods but the price or quantity is wrong: over-charges, short weights, agreed substitutions at a different price. Raise a supplier return when the problem surfaces after the driver has left: hidden damage, quality failures mid-box, wrong product discovered at prep.

Each route has one non-negotiable. A rejection must be recorded on the GRN, not just waved off the truck, or the invoice will resurrect it. A credit note must reference the GRN it corrects, or finance is matching orphaned credits at month end. A return needs its evidence attached at the moment it is raised, because a photo taken at 7am settles an argument that an email three days later cannot. The one route to ban outright is the verbal "we'll sort it on the next order", which is the least trackable object in hospitality procurement and the natural predator of every number in this article.

Closing all four leaks

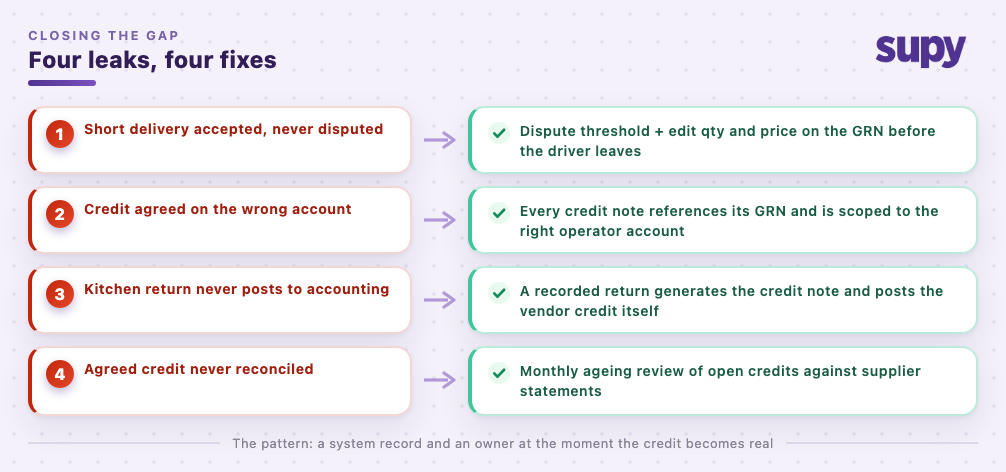

The pattern behind every fix is the same: a credit gets a system record and an owner at the moment it becomes real, not at month end. Mapped to the four points: at receiving, a dispute threshold plus the ability to edit quantity and price on the GRN turns every gap into a recorded dispute before the driver leaves. Between sites, every credit note references the GRN it corrects and is scoped to the right operator account, so it can never land somewhere its owner cannot see it. At the central kitchen, a recorded return generates the credit note and posts the vendor credit to accounting on its own, removing the manual step that kept failing. And on the statement, a monthly review of aged open credits against supplier statements catches the remainder, because a credit nobody reconciles is a credit the supplier never has to honour. Run this way, credits stop being favours to chase and become receivables with an ageing report.

Run this self-diagnostic this week: pull last month's statement from your two highest-volume suppliers for two of your sites, and count how many credits you can trace end to end, from a dispute recorded at receiving, to a credit note in your system, to a credit applied on the statement. Agreed credits with no system record mean the leak is at receiving. Credits sitting on the wrong entity mean the leak is in your account structure. Start with a receiving-time dispute threshold either way, because receiving is where credits are born or lost.

Supy's procurement suite closes all four leaks in one flow: one-tap purchase order to GRN receiving with automatic price and quantity conflict flags, credit notes raised directly against the GRN for over-charges, incorrect charges and returns, configurable dispute thresholds and per-GRN charge caps, and supplier returns that generate the vendor credit in your connected accounting system automatically, scoped to the right operator account. See how it fits your group on the restaurant procurement platform page, or start with how GRN management works across multiple sites.