.jpg)

Restaurant Expansion Strategy: What the Back of House Needs Before You Open Your Next Location

A successful restaurant expansion strategy covers more than the business case for a new site. Most expansion planning focuses on location selection, lease negotiation, and brand replication. The question that determines whether new locations stay profitable - when to build the back-of-house infrastructure for the group being built, rather than the single site already running - gets answered after the second location opens, when the gaps are already costing money.

This guide covers the operational decisions that a restaurant expansion strategy needs to resolve before opening day: food cost visibility at scale, procurement structure, central kitchen readiness, and the technology stack that makes multi-site management possible without adding operational headcount proportionally to the location count.

What Changes Operationally When You Add a Second Location

A single restaurant can run on informality. One team, one set of supplier relationships, one weekly count, and one number that represents food cost. When the owner walks the floor and checks the walk-in, they have operational visibility that no report can fully replicate. That informality works for one site.

The second location changes the picture in ways that are specific and predictable.

Inventory cannot be reconciled by walking two kitchens at different times of day, especially when the person doing the check is also managing service at the first site. Supplier relationships fragment - each location develops its own contacts, ordering cadences, and price agreements, often without anyone at group level knowing what the other is paying. The weekly count that worked for one site now takes twice as long, but the two resulting numbers cannot easily be compared because the counts were done at different times with different methods. Food cost at location two differs from location one, but the reason is not immediately obvious from the data.

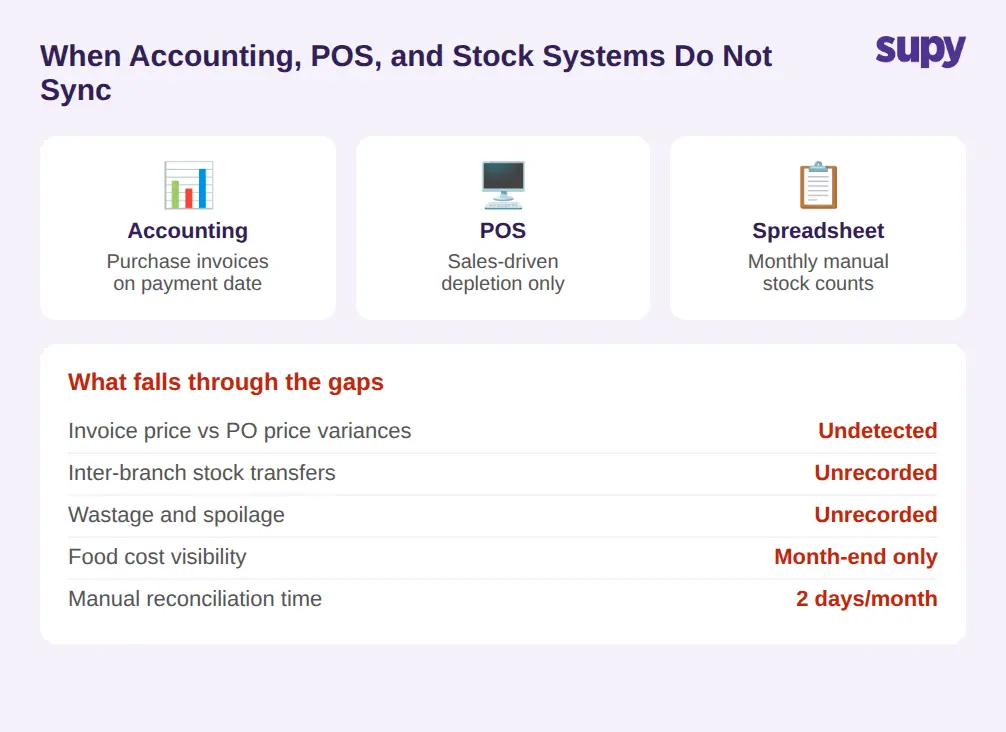

The gap that opens is in the layer between the POS and the accounting system. That middle layer - the system that tracks what ingredients should have been consumed based on what was sold and what the recipes specify, what was actually received, what was wasted, and what moved between sites - is often informal at one location. At two or more locations, the informal layer has to become explicit.

The operators who avoid the margin erosion that commonly follows early expansion are the ones who build that layer before the second site opens. The operators who build it after are the ones diagnosing food cost problems three months into the new location's operation.

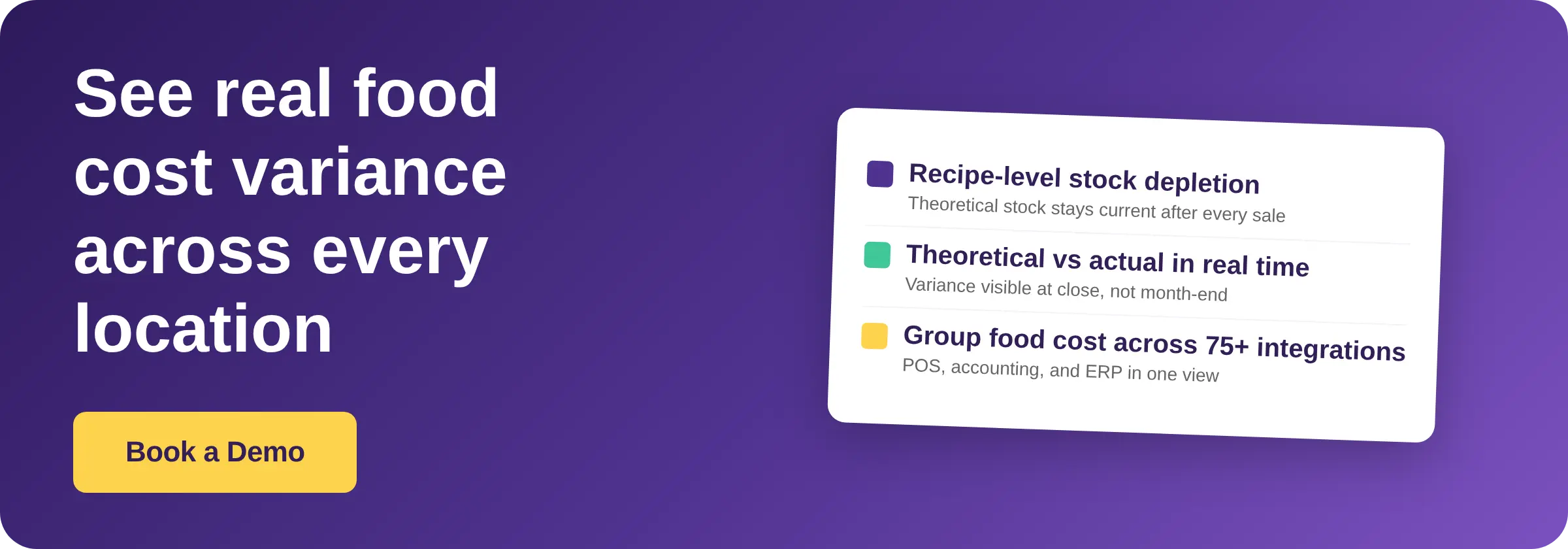

Ask: does your current back-of-house system track theoretical ingredient consumption from sales and compare it against actual usage at each site - or does it only show you a cost-of-goods figure at the end of the month?

Food Cost Control at Scale: Why Per-Location Visibility Matters More Than the Group Average

The most common food cost failure in early expansion is not that costs increase - it is that cost problems become invisible.

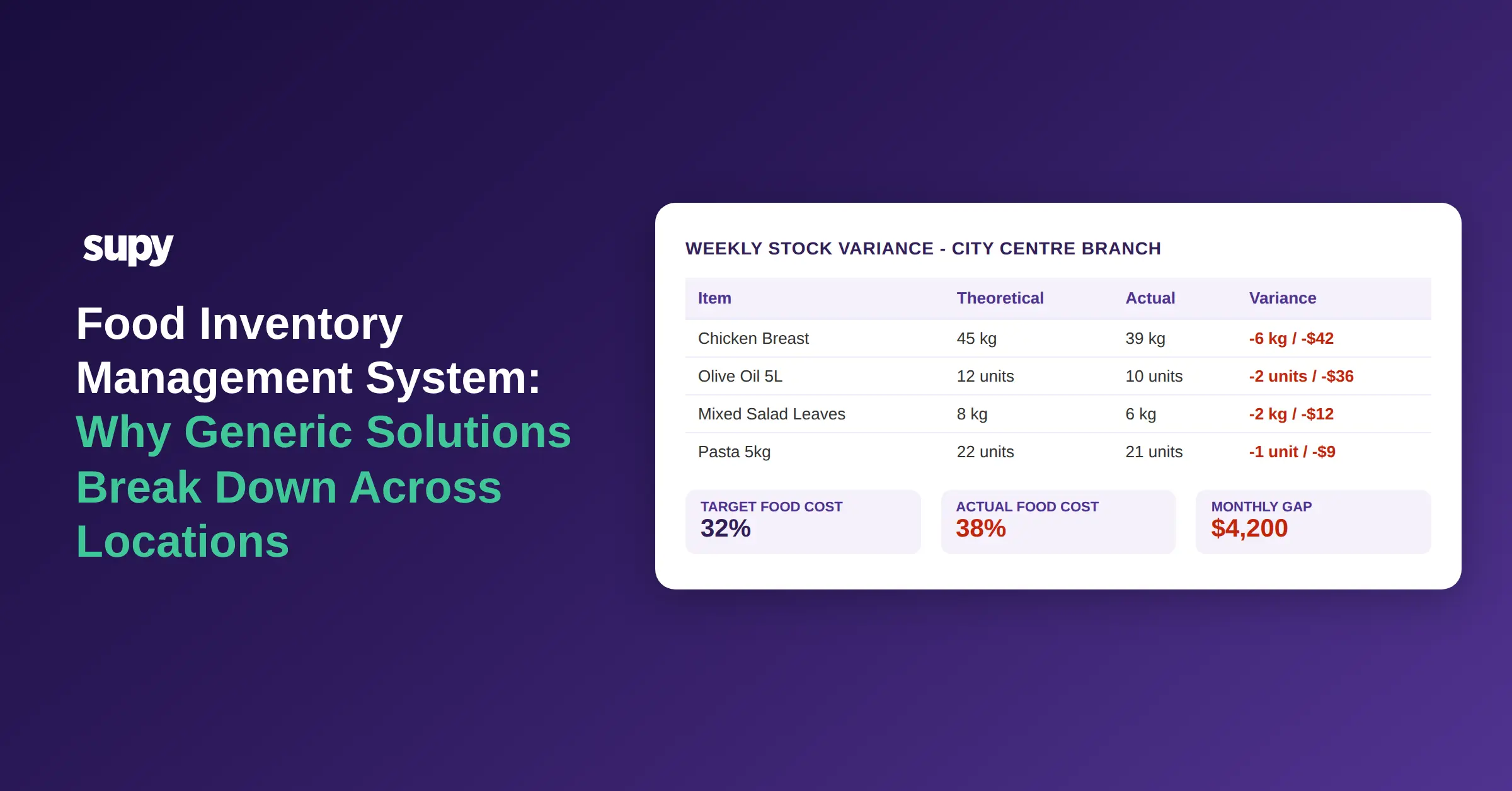

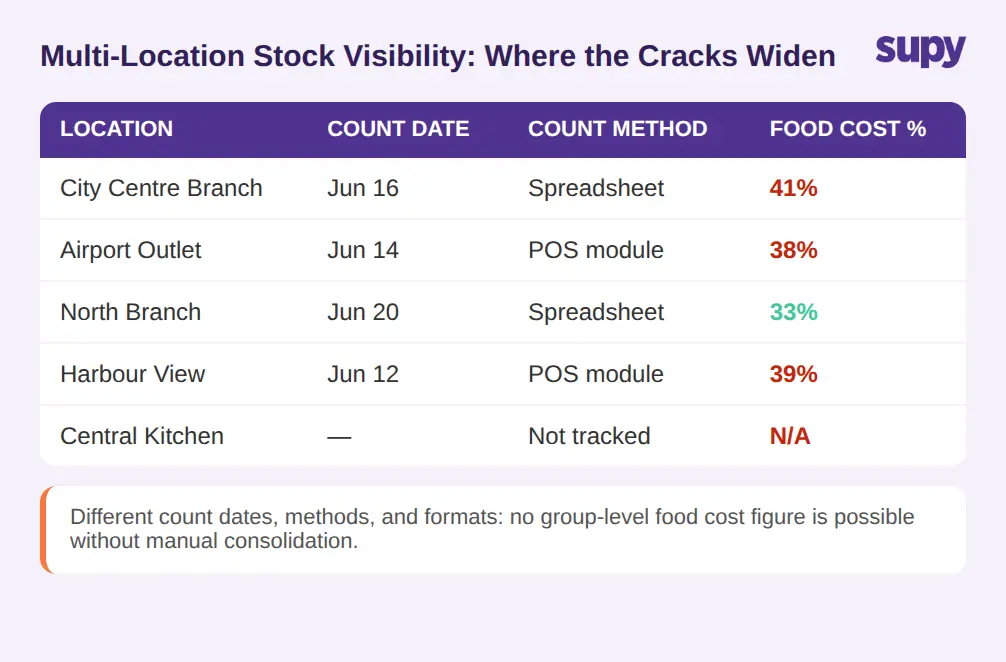

A multi-site casual dining group's finance team reported a consistent GP% of 63% across all sites. A quarterly deep-dive found two sites running between 55% and 57%. The blended group figure had masked that underperformance for 3 months. The root cause was those locations purchasing at higher prices not reflected in the recipe cost model - a gap that would have been visible in a real-time per-location report, but was invisible in the consolidated monthly figure.

The same structural problem appears in theoretical-vs-actual tracking. A multi-location fast-casual chain's head of operations found the theoretical GP% running 4-5 percentage points above the actual P&L figure. Recipe costs had not been updated in 6 months. Unrecorded spoilage and portion inconsistency were both contributing, but there was no way to isolate the dominant cause per month. The 8-point gap between what the blended figure showed and what was happening at underperforming sites is the practical cost of consolidated reporting.

Per-location theoretical-vs-actual tracking closes that window. When each site's theoretical stock is calculated from sales and recipes in real time, and compared against counted stock, the variance is visible the day it opens - not at the quarterly review. A site buying ingredients at a price the recipe model does not reflect shows a variance immediately. A site with persistent over-portioning shows a different pattern. The two are distinguishable in real time; they are not distinguishable from a blended monthly GP% figure.

Ask: can your reporting system show you the gap between theoretical and actual food cost per location, updated in real time - not as a blended group number?

Procurement at Scale: From Informal Ordering to Structured Supplier Management

At one location, procurement is typically personal. A head chef with established supplier relationships, weekly ordering by WhatsApp or phone, and an instinct for when to reorder. The model works because the person running it knows the inventory, the suppliers, and the food cost impact of every order decision.

At multiple locations, informal procurement fragments. Each site orders from its own suppliers, sometimes at different prices from the same supplier, without central oversight. A multi-location leisure and entertainment group's operations manager described having no control over stock across sites after expanding - inconsistent counts, missing items, and no visibility into losses from staff giveaways and unrecorded waste. The systems that had worked at one site had not transferred to the expanded group.

Structured procurement at multi-location scale requires three capabilities that informal ordering cannot provide. A centralised approved-supplier list, so every location orders from the same sources at agreed prices and deviations trigger a review rather than passing silently through to food cost. Spending policies and approval thresholds, so a location manager cannot place an order above a defined value without sign-off, and orders that fall outside par levels or approved suppliers are flagged before they become a cost problem. Price variance detection at goods receipt, so when a supplier invoices at a price different from the purchase order, the discrepancy is flagged before it is absorbed into cost rather than after the month-end reconciliation.

The shift from informal to structured procurement is not a step-change in effort for the individual ordering. It is a step-change in system - the same activity happens with visibility and controls that protect the group's cost model.

Ask: does your procurement system show what each location is ordering, from which suppliers, at what prices - and does it flag variances from agreed purchase order prices before they hit food cost?

The Central Kitchen Decision: What It Operationally Requires Before Opening

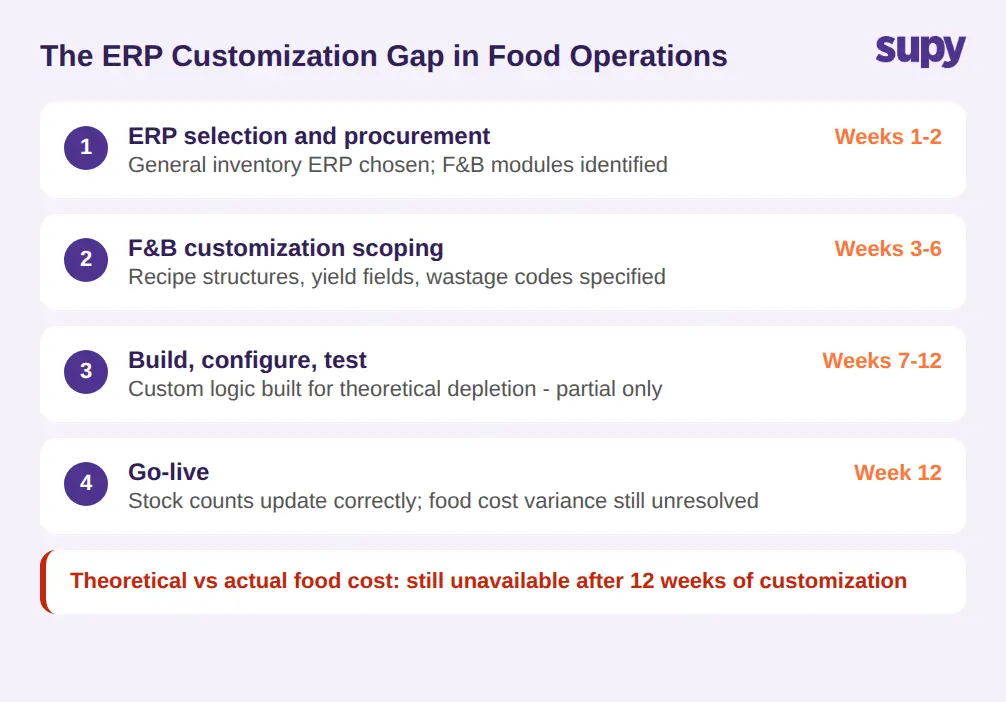

The decision to add a central kitchen is a threshold in the expansion journey. For most groups, it becomes viable at 4-6 locations - the point where standardised production at scale delivers a cost-per-dish advantage over distributed kitchen preparation. The business case is usually clear. The operational readiness requirements are frequently underestimated.

A 3-location casual dining group's chef, planning the transition to a central kitchen, expressed resistance to implementing rigorous inventory tracking - preferring to continue with an instinct-based approach. That resistance is common in owner-operated groups at the scaling inflection point. The central kitchen requires a shift from feel-based management to system-based management. A dish produced centrally for multiple branches, from shared recipes at production scale, requires bill-of-materials accuracy, transfer documentation, and delivery confirmation at every step. Without it, branch stock records are wrong from the moment the delivery arrives.

A multi-location bakery group found this practically: central kitchen items were not fully configured in the back-of-house system when the CK launched, leaving branches unable to place orders correctly. The configuration gap was not visible until branches reported shortfalls.

What the central kitchen module needs to do, operationally: receive purchase orders from any branch, consolidate cross-branch demand per ingredient or SKU, confirm and ship against a delivery note that updates stock at both the CK and the receiving branch, and handle the internal billing correctly. Central kitchen output to branches is an internal transfer - not a purchase. Back-of-house systems that treat it as a purchase double-count the cost of the item at branch level, inflating branch food cost figures.

Ask: does your back-of-house system have a dedicated central kitchen module that handles branch orders, demand consolidation, and delivery notes as internal stock movements - or would the CK be configured as an external supplier?

The Technology Stack Every Restaurant Expansion Strategy Needs

At one location, a POS and a spreadsheet cover most operational data needs. At four locations with a central kitchen, the required capability is different in kind, not just scale.

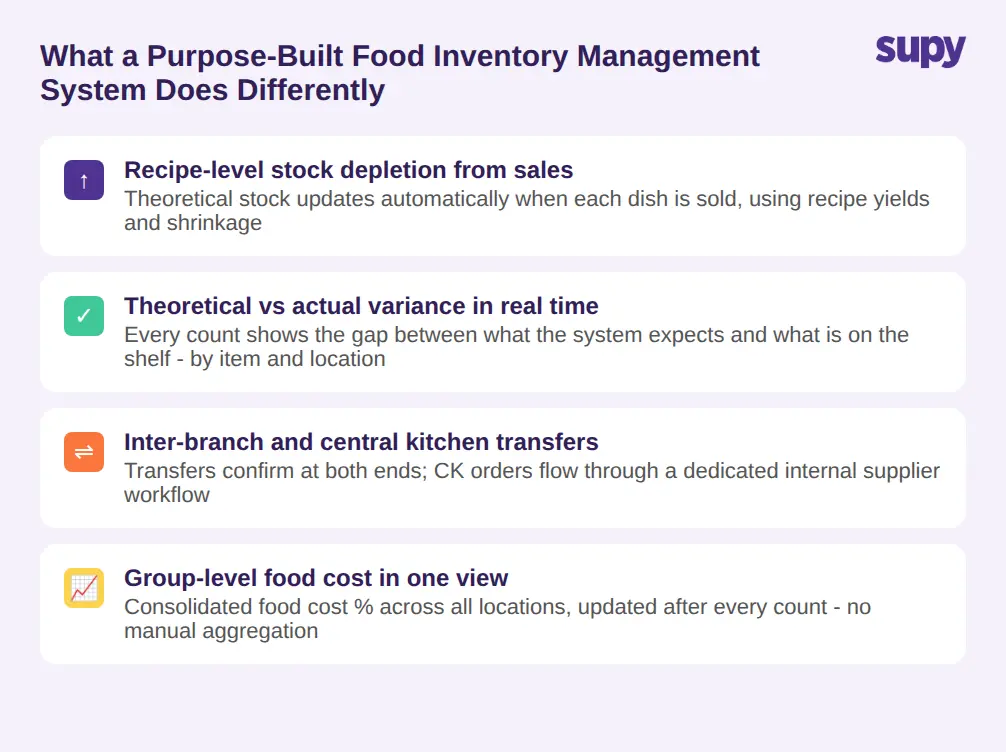

Live stock-on-hand per location and storage unit - updated continuously from every sale, receipt, transfer, and wastage log, so the theoretical stock figure is always current and comparable to a physical count. Recipe-level depletion, so every sale reduces the exact ingredients the recipe specifies, adjusted for yield and prep wastage. Inter-branch transfer workflows with a confirm-and-receive step, so stock moved between sites appears correctly in both locations' records. Centralised procurement with per-location spending policies and price variance detection. A central kitchen module if a commissary is part of the plan. And integrations with the POS and accounting systems already in use.

The integration layer matters more at scale because the reconciliation burden grows with every location. A platform that connects to 75+ POS, accounting, and ERP systems removes the manual export loop that, across multiple locations, becomes a part-time reconciliation job.

Supy's food and beverage operations platform covers all of this natively - live theoretical-vs-actual tracking by location, procurement with approval guardrails and spending policies, inter-branch transfers with a full audit trail, a central kitchen module, and 75+ integrations. Operators managing multi-location groups have reduced stock counting and reconciliation time by more than half after implementation.

The technology decision for a growing restaurant group is not about which system has the longest feature list. It is about whether the system has a coherent data model for a multi-location group - one that treats all sites, the central kitchen, and the procurement layer as a single connected operation rather than individual tools that share a login.

Ask: does your current back-of-house platform have a single data model for all your locations - or is it a collection of single-site tools that requires manual consolidation to produce a group view?

Three Questions Every Restaurant Expansion Strategy Must Answer Before the Next Opening

The operational test for expansion readiness is not whether you have the financing or the site - it is whether the back-of-house infrastructure is built for the group you are opening, not the single site you already operate.

Three questions cut through the preparation checklist:

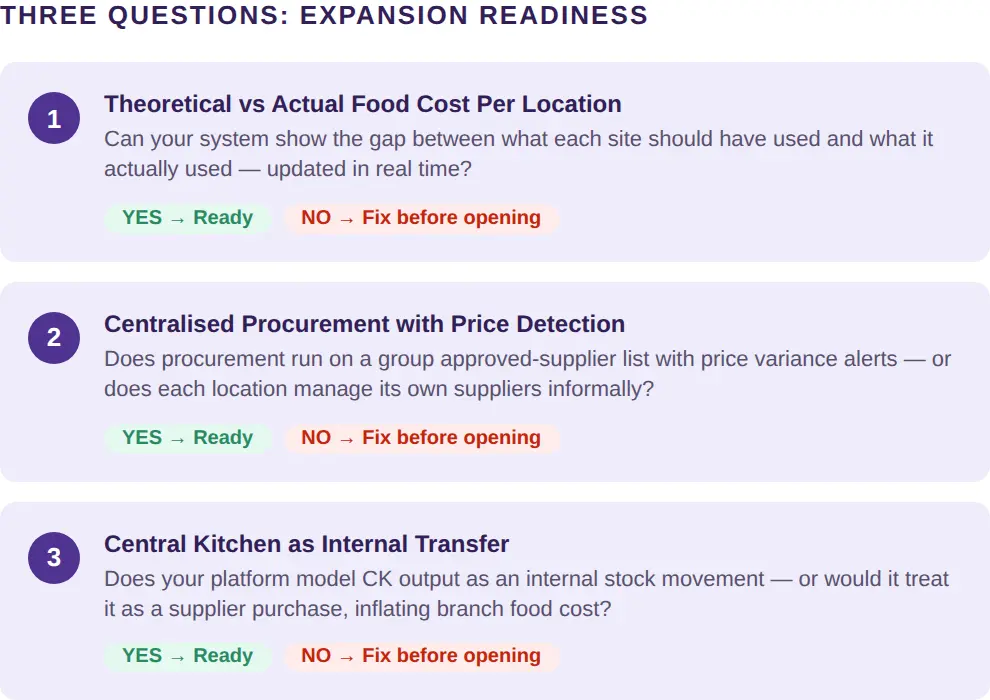

Can your system show food cost per location - theoretical versus actual - updated in real time? If not, you will not know which new site is underperforming until the damage is already visible in the quarterly review, not on the day it starts.

Does your procurement run on a centralised approved-supplier list with price variance detection, or does each location manage its own supplier relationships informally? Informal procurement scales in cost as reliably as structured procurement, but without the visibility to catch it.

If a central kitchen is part of the plan, does your back-of-house platform model CK output as an internal transfer - or would it treat it as a supplier purchase, which inflates branch food cost and breaks the cost model?

A yes to all three means the infrastructure is ready to scale. A no means the expansion will work until the second or third location reveals the gap.