.jpg)

Why Food Cost Variance Matters and How to Control It

.webp)

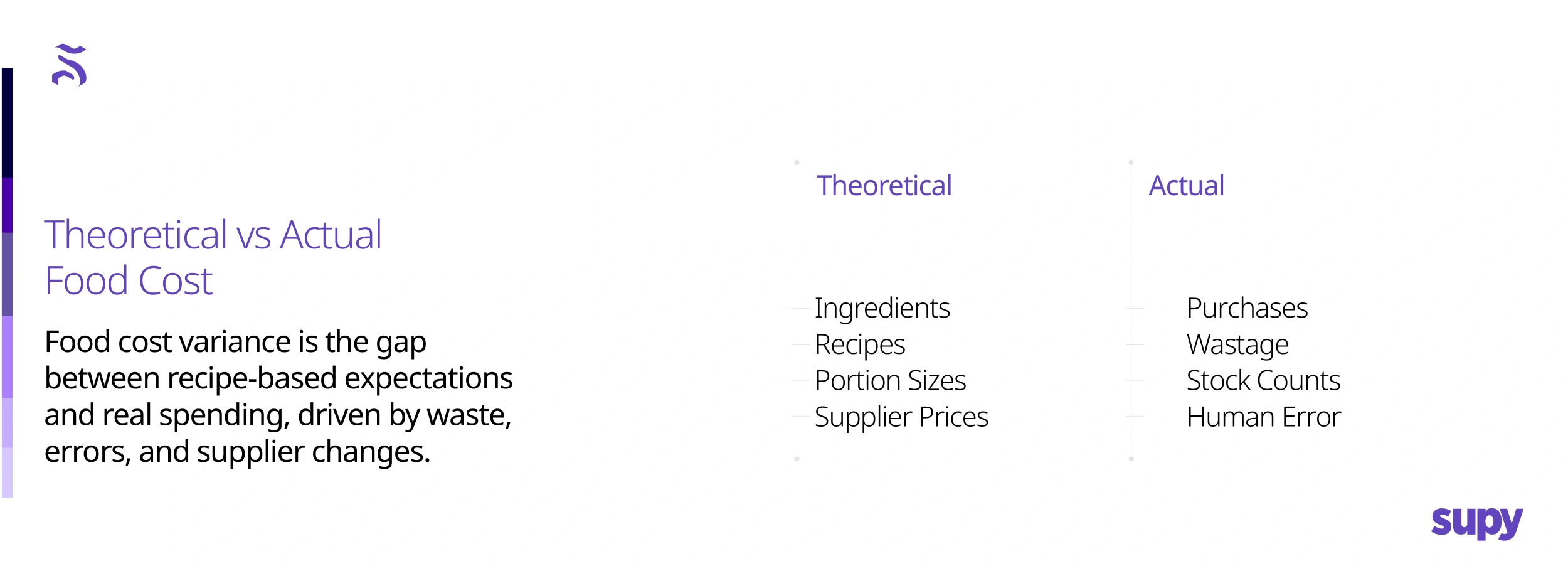

Running a multi-site restaurant network means knowing exactly how much every dish actually costs you. Theoretical food cost tells you what a recipe should cost based on ingredients and portion sizes. Actual food cost measures what you really spend once wastage, price fluctuations and human error enter the picture. The gap between these two numbers is your food cost variance, and it has a direct impact on profitability.

Many operators rely on broad averages or guesswork to gauge food cost. That approach leaves money on the table. Understanding variance – and acting on it daily – enables smart pricing, waste reduction, and better supplier negotiations. Below we answer common questions about food‑cost variance, provide practical examples, and share ways technology can keep your margins healthy.

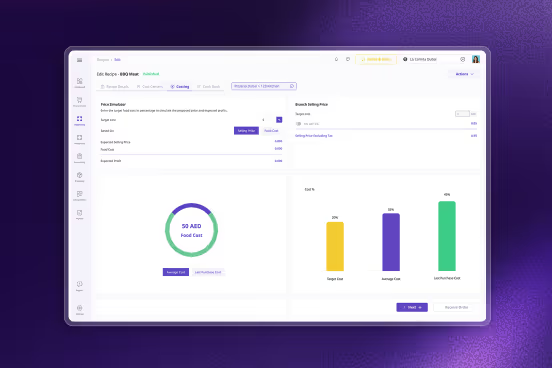

1. How does Supy calculate theoretical food cost?

Theoretical cost is built from the ground up. Every recipe is broken down by ingredient, portion size, and unit cost. Supy allows operators to input each recipe with precise weights and measurements. It then multiplies these by the most up‑to‑date supplier prices and yields a per‑dish cost. When ingredients are blended or prepped in‑house (think sauces or breads), Supy traces the cost of each component back to the finished item.

The result is a clean benchmark for what the food should cost if portion sizes are accurate and there is no waste. This benchmark is the starting point for measuring variance and deciding if prices or recipes need to change.

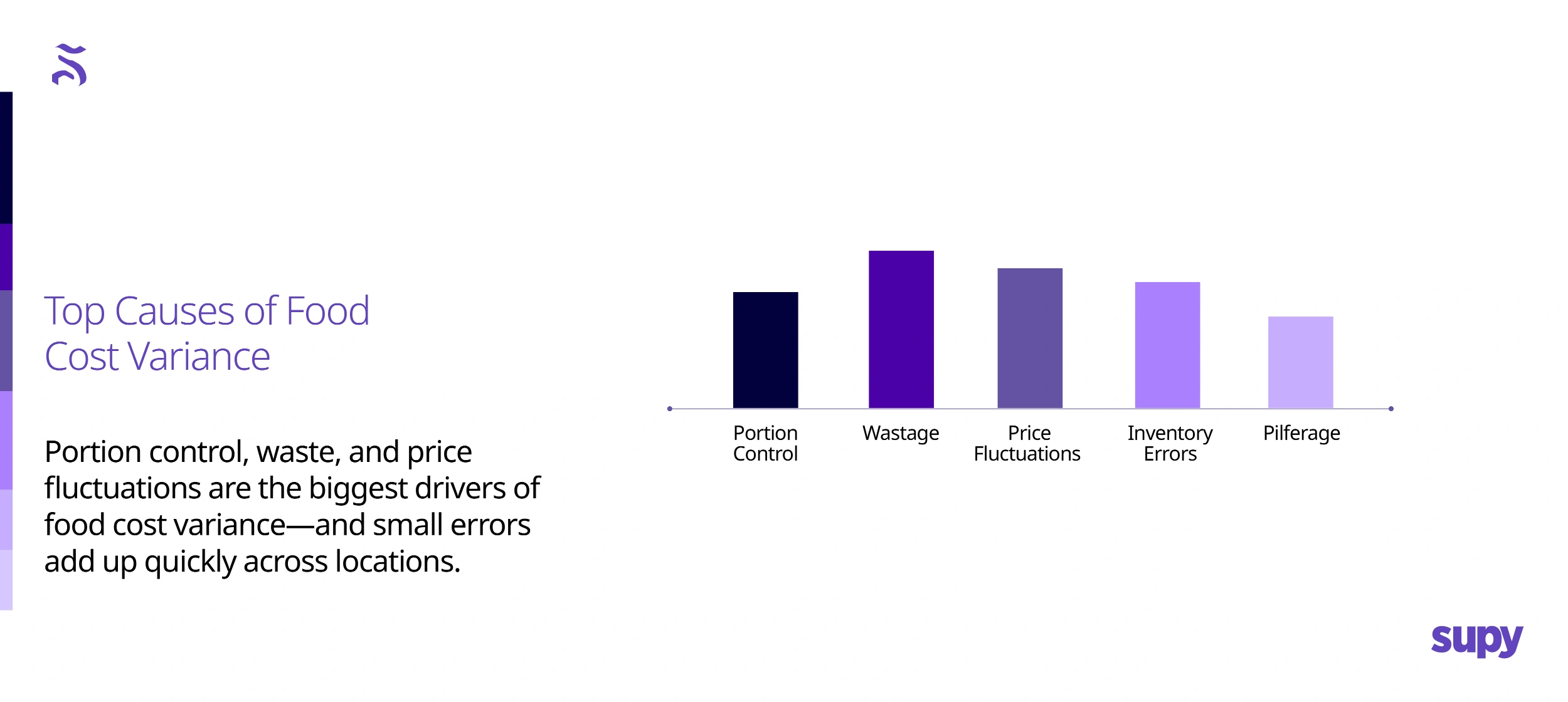

2. What causes variance between actual and theoretical food cost?

The most common drivers of food‑cost variance include:

- Portion control – Over‑scooping ice cream or adding extra slices of cheese quickly erodes margins.

- Wastage – Spoiled or accidentally dropped product increases actual cost without revenue to offset it.

- Price changes – Rising supplier costs may not be reflected in the theoretical benchmark if recipes aren’t updated.

- Inventory inconsistencies – Manual stock counts and mis‑allocated transfers create discrepancies.

- Pilferage – Missing inventory often shows up as inflated actual cost.

A small error in each area compounds over multiple locations. That’s why disciplined daily processes and data are critical.

3. How does recipe costing tie into variance tracking?

Consistent recipe costing is the backbone of variance control. In Supy, each recipe’s ingredients, quantities and yields are logged. When a recipe changes – adding a new garnish or switching to a different beef supplier – the cost automatically updates across all relevant dishes.

This granular recipe data feeds into theoretical cost. When you later compare the theoretical cost with actual food spend from invoices and stock counts, the system flags differences. Without accurate recipe costings, variance analysis becomes guesswork.

4. What role does wastage tracking play in variance reduction?

Wastage directly raises actual food cost. Supy lets teams log spoilage or prep errors as they happen. For example, if a batch of soup is over‑seasoned and thrown away, staff can record the loss against the relevant cost centre. Over time, this data highlights trends – perhaps a supplier’s produce has a shorter shelf life, or an inexperienced prep team is trimming too much fat off steaks.

By pairing wastage logs with theoretical cost, operators can target training or renegotiate with suppliers. Reducing waste shrinks the variance and keeps COGS in check.

5. How do supplier price fluctuations affect actual food cost?

If cheese prices jump 20 % and you don’t adjust your recipes or menu prices, the theoretical cost becomes outdated. Supy solves this by linking supplier invoices directly to ingredient costs. When a price change comes in, operators see the effect on each dish. They can either update the selling price, alter portion sizes or substitute ingredients. Keeping theoretical cost current ensures variance reports remain meaningful.

6. Can Supy auto‑flag discrepancies for managers?

Yes. Supy’s variance dashboard compares theoretical versus actual cost for each location and category. When a variance exceeds a threshold (say ±5 %), the system flags it and highlights the likely causes – such as unusual wastage or a recent price change. Notifications can be sent to managers so they investigate immediately, rather than discovering problems at month‑end.

7. How often do operators check variance – daily, weekly, monthly?

High‑performing operators monitor variance at least weekly. Daily checks are common for perishable categories like produce or seafood. Supy allows rolling variance reports so managers see trends early and don’t wait until the end of the period when it’s harder to course‑correct. Reviewing variance weekly also means corrective actions (training, price adjustments) happen in near real‑time.

8. How do credit notes help control variances?

Credit notes offset invoiced costs when suppliers deliver short or poor‑quality goods. For instance, if a box of tomatoes arrives bruised and you can only use half, you issue a credit. Supy logs credit notes against the relevant ingredient, lowering actual cost. Without credit notes recorded, the variance will show up as higher actual cost. Over time, credit notes help identify problematic suppliers or packaging methods.

9. Can you share an example of variance savings from a client?

One multi‑unit bakery noticed a 4 % variance on flour. The theoretical cost assumed 1 kg of flour produced 20 baguettes. After conducting a line check, they discovered bakers were rounding up each portion by 10 g, meaning each baguette used slightly more flour. Over a week, that translated to 25 kg of unaccounted flour per location. By training staff to weigh portions accurately and adjusting the recipe yield, the variance fell to under 1 %. The cost savings across ten stores amounted to thousands of dollars per month.

Another example: a casual dining chain saw its chicken wing variance spike after switching suppliers. The new wings were smaller, prompting cooks to add extra pieces to reach plating weight. By renegotiating with the supplier and adjusting portion counts, the variance returned to target.

10. What future improvements are being planned for variance tracking?

Future developments focus on predictive variance and real‑time action. This includes:

- AI‑driven forecasting to suggest menu price changes before variance spikes.

- Automated supplier sourcing to recommend alternative vendors when costs rise.

- Deeper waste categorisation linking prep mistakes to training modules.

- Improved mobile workflows for logging waste and credit notes on the fly.

These enhancements will give operators earlier visibility and tools to act pre‑emptively, further narrowing the gap between theoretical and actual cost.

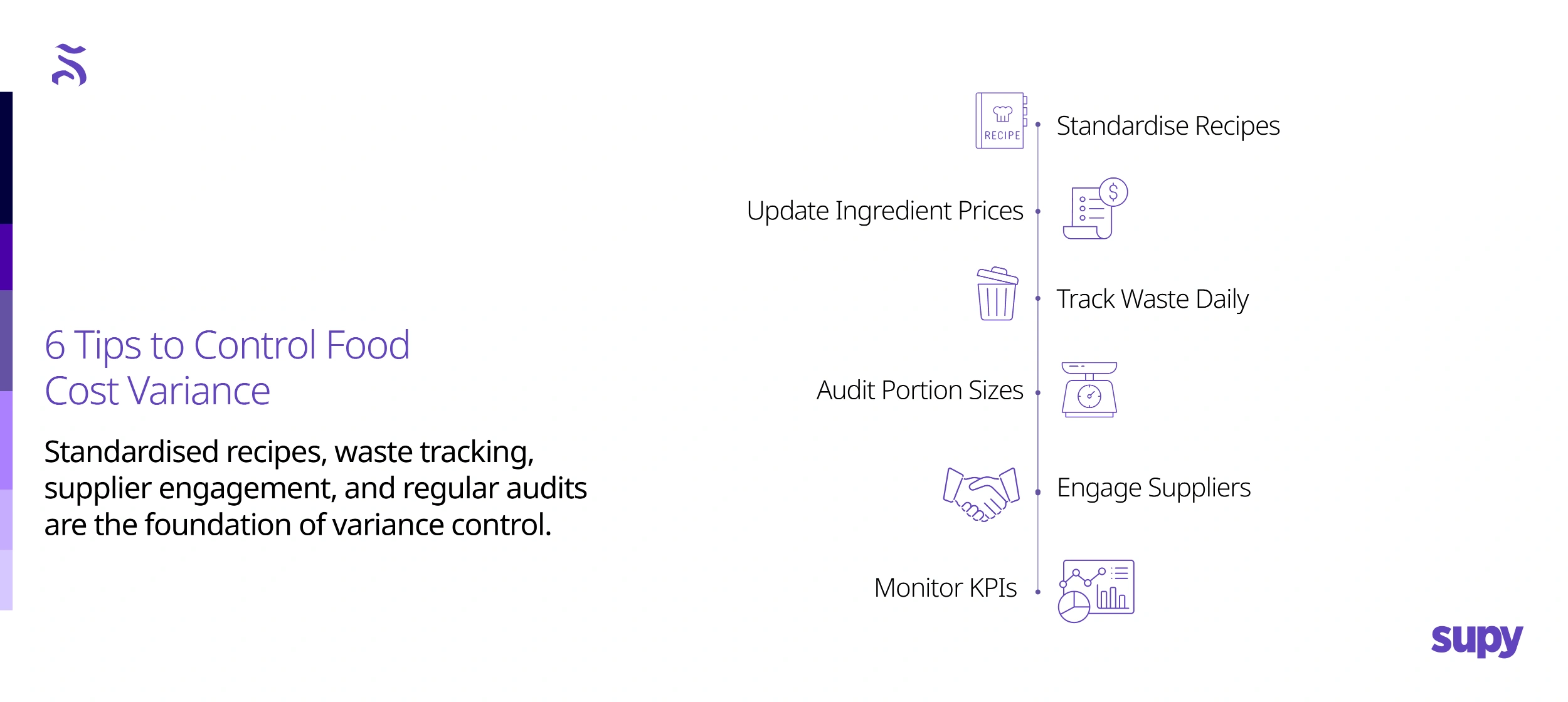

Practical Tips for Controlling Food Cost Variance

- Standardise recipes – ensure every location uses the same portions and ingredients. Document them clearly and train staff.

- Update ingredient prices promptly – sync your supplier invoices so theoretical costs stay relevant.

- Track waste daily – use simple forms or mobile apps to record what gets thrown away and why.

- Audit portion sizes – conduct random checks and use measuring tools where possible.

- Engage suppliers – negotiate better pricing, credit for poor quality, or alternative products when costs rise.

- Monitor KPIs – beyond variance percentage, track sales mix, wastage ratios, and price elasticity.

Conclusion

If controlling food cost variance is keeping you up at night, you’re not alone. Successful operators use smart systems like Supy to automate recipes, monitor wastage and spot problems before they hit the P&L.

- Explore more best practices – Check out this guide to menu engineering for multi‑unit operators for additional insights on pricing and product mix.

Book a demo – Curious how Supy can make variance management painless? Book a demo and see for yourself.

Related Resources

- Podcast: Supply Chain Director : This Is What Builds Profitable Businesses (Tashas Group)

- 10 Tips To Reduce Restaurant Food Waste

- The Ultimate Guide To Restaurant Operations Management

Related Resources